Part 2/3: Why Good Solar Projects Don't Get Approved

by Fredrik Hagelberg, MD, IBC SOLAR

A common question asked by businesses considering solar is:"What is the best way to fund my project?" There is no easy answer.

What is, however, increasingly common for businesses is the desire to reduce energy costs, mitigate operational risk and leverage 3rd party finance to do it.

More than 50% of C&I solar projects are now being implemented through off-balance-sheet financing structures, predominantly via PPAs

There is no universally superior funding structure. The most appropriate solution depends on the organisation's financial position, strategic priorities, appetite for ownership and approach to risk management, especially when it comes to utilities.

Unfortunately, many solar proposals still focus almost entirely on technical specifications and projected energy yields while giving limited attention to the financial structure itself.

This is a missed opportunity.

For many businesses, a solar PV project funding model is ultimately more important than the technology installed. As long as certain fundamentals are addressed, including product warranties and performance guarantees, businesses will value the financial merits of the solution alongside the energy savings.

Traditionally, solar projects were purchased outright. A business would fund the CAPEX and own the asset outright and benefit directly from all future electricity savings. This approach remains attractive for organisations with strong cash reserves and a long-term investment horizon.

Ownership generally delivers the lowest lifetime energy cost and allows businesses to benefit from accelerated depreciation incentives where applicable (such as SARS 12B). Over the life of the system, outright ownership often produces the highest financial return.

System ownership requires substantial upfront investment and places ongoing maintenance, operational and performance responsibilities on the asset owner.

When I have had the opportunity to ask business owners of solar systems they have installed, “How much money and energy have you saved since installing the solar system?” more often than not, they have no idea. This clearly demonstrates the importance of managing this type of asset. Any ROI shared in a proposal with a client is purely theoretical. Managing a solar asset requires specialisation and consistent management to achieve savings.

This is why many businesses are considering alternative funding mechanisms aside from traditional bank finance, which is usually just debt or asset finance. They want the savings without the risks of ownership.

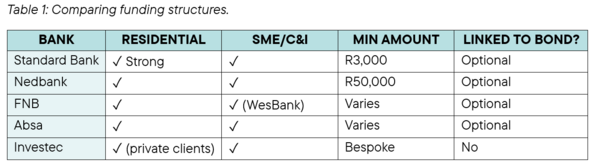

Before exploring alternative funding structures, it's worth noting that South Africa's major commercial banks also offer solar-specific financing products.

Table 1 provides a quick comparison.

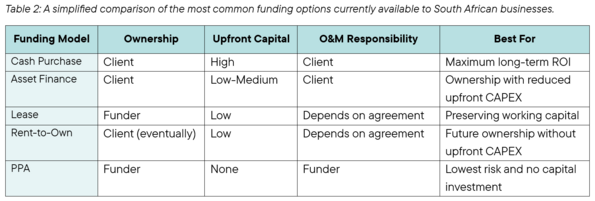

While outright ownership and traditional bank finance remain viable options for many businesses, an increasing number of organisations are exploring alternative funding structures that reduce upfront capital requirements and transfer some of the risks associated with ownership.

Table 2 provides a simplified comparison of the most common funding options currently available to South African businesses considering solar PV investments.

Lease Agreements

Under a lease arrangement, the solar system is financed through fixed monthly payments over an agreed term. The business gains immediate access to the benefits of solar without the need for significant upfront capital expenditure.

For many SMEs, leasing can be particularly attractive because it preserves working capital while still reducing monthly electricity spend.

Instead of investing millions into infrastructure, capital remains available for business operations, expansion initiatives and strategic investments.

Rent-to-own

Rent-to-own structures occupy an increasingly important position within the market.

These arrangements combine many of the benefits of leasing with the long-term advantages of ownership.

The customer makes monthly payments over a defined period and ultimately acquires ownership of the asset at the conclusion of the agreement.

This approach often appeals to organisations that want to own the system eventually but prefer to avoid CAPEX upfront.

Power Purchase Agreements (PPAs)

PPAs represent a fundamentally different approach.

Under a PPA, the customer does not purchase the solar system at all. Instead, the customer purchases electricity generated by the system at a predetermined rate.

The solar asset remains owned by the investor or funding partner.

From the customer's perspective, this can be highly attractive.

No CAPEX needed. Maintenance responsibilities are the system owner's. Performance risks are often managed contractually. The customer simply consumes electricity at an agreed tariff that is generally lower than the grid electricity price.

This model has become increasingly popular among larger commercial and industrial energy users seeking to preserve capital while reducing operating costs.

The rapid growth of independent power producers and energy-as-a-service providers across South Africa reflects this trend.

A common mistake is comparing the cost of a PPA directly to the return on an owned system. These solutions solve different problems. Ownership focuses on maximising long-term return, while a PPA focuses on reducing energy costs without requiring capital investment, transferring operational risk and simplifying energy management.

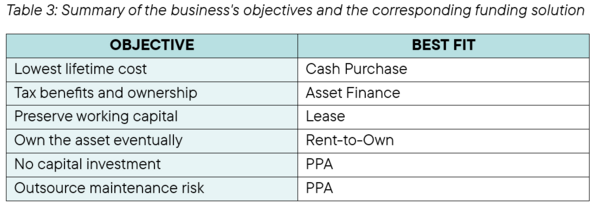

Table 3 summarises some of the business's objectives and the corresponding funding solution.

Importantly, the choice between these models should not be driven solely by monthly cost comparisons.

Businesses should evaluate several factors, including capital availability, borrowing capacity, tax considerations, risk appetite, operational capabilities and long-term strategic objectives.

- A manufacturing company seeking maximum long-term returns may favour ownership.

- A logistics company prioritising capital preservation may prefer leasing.

- A property owner looking to improve tenant retention may explore rent-to-own structures.

- A national retail group seeking predictable energy costs may find a PPA most attractive.

The critical lesson is that solar financing should be aligned with business strategy rather than simply product availability.

The most successful solar projects are often not those with the lowest equipment costs. They are the projects where the funding structure aligns perfectly with the customer's financial objectives.

You should also consider the various funders’ appetite for certain market sectors. Some will not entertain any agricultural businesses, while others specialise in that segment. Some will have minimum CAPEX value thresholds to justify their involvement. You will need to reach out to each to understand what their project preferences are as well as their risk appetite. You will find that the alternative funders are more flexible in their approach and are negotiable.

For example, some PPA offers will have annual CPI+1 or 2% tariff interest rates. These rates and tariffs can be adjusted if the term of the contract changes from 10 to 15 or 20 years.

Some will offer a fixed monthly fee for a BESS system, whereas the PV portion will be on a variable rate. The term for each asset in the same contract might even differ. You might have a 10-year contract for the entire system, including BESS, or it might be split into 10 years for BESS and 20 years for PV, for the same system.

In some cases, a funder might even be prepared to include additional project costs such as upgrading a roof or adding security fencing and cameras. The cost can be included in the project and be part of the PPA tariff for example.

An oft-forgotten benefit for an installer when successfully closing a funded deal is the ongoing revenue through an O&M contract with the IPP. This could even be maintained for the life of the project if cost-effective. This is where outright purchases of systems don’t benefit the installer – they might not enjoy the annuity income from offering an additional service.

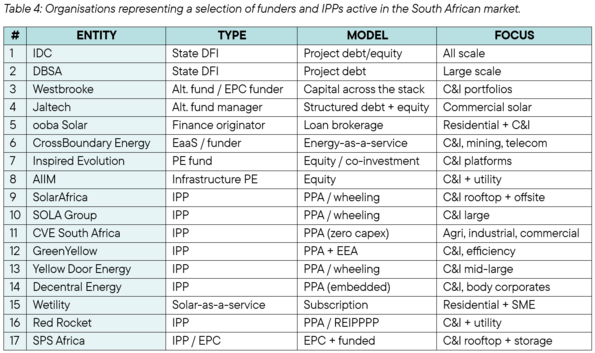

Below is a selection of C&I-focused IPPs and specialist non-bank funders that are actively supporting solar PV deployments in South Africa. While funding appetite varies between institutions, all will conduct a detailed assessment of the opportunity before committing capital. This typically includes evaluating the installer's technical and operational capability, the end-user's credit standing, the quality and performance assumptions of the proposed system, and the overall risk profile and bankability of the project.

The organisations in Table 4 represent a selection of funders and IPPs active in the South African market.

This is not an exhaustive list and funding appetite changes over time.

Finally, and probably one of the most important considerations when presenting a funded solution to a prospective client (and this is especially true of PPAs) is to clearly communicate the fundamental difference between investing in a system outright or utilising 3rd party funding. Outright ownership offers a Return on Investment (ROI) compared to a funded solution, which offers predictable, lower energy costs, mitigates operational risk and acts like a utility.

The best funding model is rarely the cheapest one. The best funding model is the one that aligns most closely with the customer's financial objectives, risk profile and operational priorities. Installers who understand these differences are better positioned to guide clients towards solutions that get approved and ultimately implemented. In the next article, we explore what the future might hold, including the influence of AI in project design and funding.